Fill a Valid Iowa Ia 1040C Template

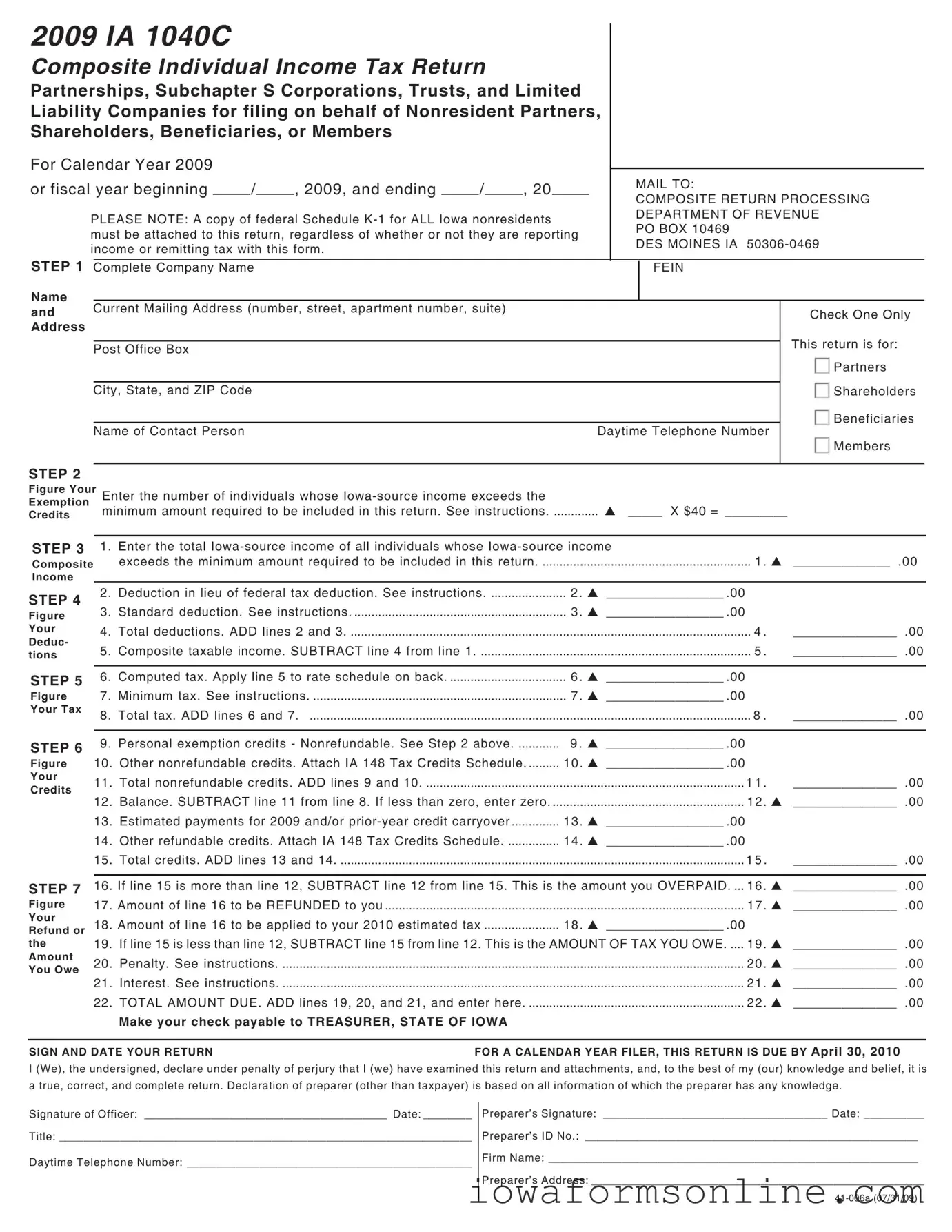

The Iowa IA 1040C form serves as a composite individual income tax return designed specifically for partnerships, Subchapter S corporations, trusts, and limited liability companies. This form allows these entities to file on behalf of nonresident partners, shareholders, beneficiaries, or members who earn income from Iowa sources. Filing this return is crucial for those who do not meet the minimum income requirements to file individually. To ensure compliance, a copy of federal Schedule K-1 must accompany the IA 1040C, detailing each nonresident's income and modifications. The form guides users through several steps, including calculating exemption credits, deductions, and tax liabilities, ultimately determining any refund or amount owed. Understanding the specific requirements and deadlines, such as the due date of April 30 for calendar year filers, is vital for accurate and timely submission. Additionally, the form outlines penalties for late filing or underpayment, emphasizing the importance of thorough preparation and adherence to Iowa tax regulations.

Iowa Ia 1040C Preview

2009 IA 1040C

Composite Individual Income Tax Return

Partnerships, Subchapter S Corporations, Trusts, and Limited

Liability Companies for filing on behalf of Nonresident Partners,

Shareholders, Beneficiaries, or Members

For Calendar Year 2009 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

MAIL TO: |

||

or fiscal year beginning |

|

/ |

|

, 2009, and ending |

|

/ |

|

, 20 |

|

|

||

|

|

|

|

|

|

COMPOSITE RETURN PROCESSING |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

PLEASE NOTE: A copy of federal Schedule |

|

DEPARTMENT OF REVENUE |

||||||||||

|

PO BOX 10469 |

|||||||||||

must be attached to this return, regardless of whether or not they are reporting |

|

|||||||||||

|

DES MOINES IA |

|||||||||||

income or remitting tax with this form. |

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

||

STEP 1 Complete Company Name |

|

|

|

|

|

|

|

|

FEIN |

|||

Name

and Current Mailing Address (number, street, apartment number, suite)Check One Only

Address

Post Office Box |

|

This return is for: |

|||

|

|

|

|

|

|

|

|

|

|

|

Partners |

|

|

|

|

|

|

City, State, and ZIP Code |

|

|

|

|

Shareholders |

|

|

|

|

|

Beneficiaries |

|

|

|

|

|

|

|

|

|

|

|

|

Name of Contact Person |

Daytime Telephone Number |

|

|

||

|

|||||

|

|

|

|

|

Members |

STEP 2

Figure Your

Exemption

Credits

Enter the number of individuals whose |

|

minimum amount required to be included in this return. See instructions |

_____ X $40 = _________ |

STEP 3 |

1. Enter the total |

|

|

Composite |

exceeds the minimum amount required to be included in this return |

1 . |

______________ . 00 |

Income

STEP 4

Figure Your Deduc- tions

STEP 5

Figure Your Tax

STEP 6

Figure

Your

Credits

STEP 7

Figure Your Refund or the Amount You Owe

2. |

Deduction in lieu of federal tax deduction. See instructions |

2 . |

_________________ .00 |

|

|

|

3. |

Standard deduction. See instructions |

3 . |

_________________ .00 |

|

|

|

4. |

Total deductions. ADD lines 2 and 3 |

|

4 . |

_______________ |

.00 |

|

5. |

Composite taxable income. SUBTRACT line 4 from line 1 |

|

5 . |

_______________ |

.00 |

|

|

|

|

|

|

|

|

6. |

Computed tax. Apply line 5 to rate schedule on back |

6 . |

_________________ .00 |

|

|

|

7. |

Minimum tax. See instructions |

7 . |

_________________ .00 |

|

|

|

8. |

Total tax. ADD lines 6 and 7. ................................................................................................................................. 8 . |

_______________ |

.00 |

|||

|

|

|

|

|

|

|

9. |

Personal exemption credits - Nonrefundable. See Step 2 above |

9 . |

_________________ .00 |

|

|

|

10. |

Other nonrefundable credits. Attach IA 148 Tax Credits Schedule |

10 . _________________ .00 |

|

|

|

|

11. |

Total nonrefundable credits. ADD lines 9 and 10 |

|

1 1 . |

_______________ |

.00 |

|

12. |

Balance. SUBTRACT line 11 from line 8. If less than zero, enter zero |

|

12 . |

_______________ |

.00 |

|

13. |

Estimated payments for 2009 and/or |

13 . _________________ .00 |

|

|

|

|

14. |

Other refundable credits. Attach IA 148 Tax Credits Schedule |

14 . _________________ .00 |

|

|

|

|

15. |

Total credits. ADD lines 13 and 14 |

|

1 5 . |

_______________ |

.00 |

|

|

|

|

|

|

||

16. |

If line 15 is more than line 12, SUBTRACT line 12 from line 15. This is the amount you OVERPAID. ... |

16 . |

_______________ |

.00 |

||

17. |

Amount of line 16 to be REFUNDED to you |

|

17 . |

_______________ .00 |

||

18. |

Amount of line 16 to be applied to your 2010 estimated tax |

18 . _________________ .00 |

|

|

|

|

19. |

If line 15 is less than line 12, SUBTRACT line 15 from line 12. This is the AMOUNT OF TAX YOU OWE |

19 . |

_______________ |

.00 |

||

20. |

Penalty. See instructions |

|

20 . |

_______________ |

.00 |

|

21. |

Interest. See instructions |

|

21 . |

_______________ |

.00 |

|

22. |

TOTAL AMOUNT DUE. ADD lines 19, 20, and 21, and enter here |

|

22 . |

_______________ .00 |

||

|

Make your check payable to TREASURER, STATE OF IOWA |

|

|

|

|

|

SIGN AND DATE YOUR RETURN |

FOR A CALENDAR YEAR FILER, THIS RETURN IS DUE BY April 30, 2010 |

I (We), the undersigned, declare under penalty of perjury that I (we) have examined this return and attachments, and, to the best of my (our) knowledge and belief, it is a true, correct, and complete return. Declaration of preparer (other than taxpayer) is based on all information of which the preparer has any knowledge.

Signature of Officer: ________________________________________ Date: ________

Title: ____________________________________________________________________

Daytime Telephone Number: _______________________________________________

Preparer’s Signature: _____________________________________ Date: __________

Preparer’s ID No.: _______________________________________________________

Firm Name: _____________________________________________________________

Preparer’s Address: _______________________________________________________

Instructions for Composite Iowa Individual Income Tax Return

Election of Composite Filing

Composite returns for the 2009 calendar year must be filed by April 30, 2010. An automatic

Filing Requirements

Nonresident partners, shareholders, members, or beneficiaries cannot be included in a composite return if the nonresident does not have more income from Iowa sources than the amount of one standard deduction for a single taxpayer plus an amount of income necessary to create a tax liability at the effective tax rate on the composite return sufficient to offset one personal exemption. See minimum filing requirements below under line 6.

In addition, the above individuals should not be included if they have incomes from Iowa sources other than from the partnership or other entity; these individuals are required to file Iowa individual income tax returns.

Line Instructions

1.Each nonresident partner’s, shareholder’s, or member’s Iowa

IA 1040C.

Beneficiaries of a trust do not have an Iowa

2.A deduction is allowed in lieu of the deduction for federal tax paid and is based upon the following schedule:

Amount shown on line 1 |

|

Deduction |

||

0 |

- |

$49,999 = |

No deduction |

|

$50,000 |

- |

$99,999 |

= |

5% of line 1 |

$100,000 |

- |

$199,999 |

= |

10% of line 1 |

Over |

$200,000 |

= |

15% of line 1 |

|

3.For 2009 the standard deduction allowed is the lesser of $1,780 or the income attributable to Iowa of the partner, shareholder, or member filing this composite return.

|

|

TAX RATE SCHEDULE |

|

|

|

|

|

|

|

But |

|

|

|

|

Of Excess |

Minimum |

Over |

Not Over |

|

|

Tax Rate |

|

Over |

Income |

$0 |

$1,407 |

$0.00 |

+ |

(0.36% |

x |

$0) |

Filing |

$1,407 |

$2,814 |

$5.07 |

+ |

(0.72% |

x |

$1,407) |

Requirement |

$2,814 |

$5,628 |

$15.20 |

+ |

(2.43% |

x |

$2,814) |

$2,669 |

$5,628 |

$12,663 |

$83.58 |

+ |

(4.50% |

x |

$5,628) |

$2,434 |

$12,663 |

$21,105 |

$400.16 |

+ |

(6.12% |

x |

$12,663) |

$2,397 |

$21,105 |

$28,140 |

$916.81 |

+ |

(6.48% |

x |

$21,105) |

$2,368 |

$28,140 |

$42,210 |

$1,372.68 |

+ |

(6.80% |

x |

$28,140) |

$2,285 |

$42,210 |

$63,315 |

$2,329.44 |

+ |

(7.92% |

x |

$42,210) |

$2,225 |

$63,315 |

over |

$4,000.96 |

+ |

(8.98% |

x |

$63,315) |

|

|

|

|

|

|

|

|

6.Use the tax rate schedule above to figure your tax on composite Iowa taxable income. Also listed are the minimum requirements for each tax rate.

7.Partners, shareholders, or members reporting income on the composite return may also be subject to Iowa minimum tax. The Iowa alternative minimum tax is imposed on most of the same tax preference and adjustment items treated as exclusions as for federal alternative minimum tax purposes. Please see form IA 6251 to determine if any Iowa minimum tax is due, and attach completed form if necessary.

9.Personal exemption credits for 2009 for each partner, shareholder or member is $40.

10.Enter the total of the nonrefundable credits from the IA 148 Tax Credits Schedule. The IA 148 Tax Credits Schedule must be attached.

13.Enter the total amount of 2009 estimated tax payments and any of the prior year’s refund applied to your estimated payments for 2009.

Although estimated payments are not required, 2010 estimated payments may be made on form IA 1040ES using the partnership’s, limited liability company’s, S corporation’s, or trust’s identification number.

14.Enter the total of the refundable credits from the IA 148 Tax Credits Schedule. Attach the IA 148 Tax Credits Schedule.

20.If you do not mail your return by the due date and at least 90% of the correct tax is not paid, you owe an additional 10% of the tax due. If you file your return on time but do not pay at least 90% of the correct tax due, you owe an additional 5% of the tax due.

21.Interest is added at a rate of 0.4% per month beginning on the due date of the return and accrues each month until payment is made.

Preparer’s ID Number

Enter preparer’s SSN, FEIN, or PTIN.

Document Attributes

| Fact Name | Details |

|---|---|

| Purpose of the Form | The IA 1040C form is used for filing a composite individual income tax return on behalf of nonresident partners, shareholders, beneficiaries, or members of partnerships, S corporations, trusts, and limited liability companies. |

| Filing Deadline | For the 2009 tax year, the composite return must be filed by April 30, 2010. An automatic six-month extension is available if 90% of the tax due is paid by the original due date. |

| Required Attachments | A copy of federal Schedule K-1 for all Iowa nonresidents must be attached to the return, regardless of whether they are reporting income or remitting tax. |

| Minimum Income Requirement | Nonresident partners, shareholders, or members cannot be included in a composite return unless their Iowa-source income exceeds the amount of one standard deduction plus an amount necessary to create a tax liability sufficient to offset one personal exemption. |

| Governing Law | The IA 1040C form is governed by Iowa Code Section 422, which outlines the regulations surrounding individual income tax returns in Iowa. |

Popular PDF Forms

Iowa 470 0040 - Correct previously entered data or add new details to Medicaid claims seamlessly with the efficient Iowa 470 0040 form.

For those interested in safeguarding themselves, utilizing a Hold Harmless Agreement form is crucial, and you can find a reliable template at Texas Documents to ensure all necessary details are covered accurately.

How to Win a Termination of Parental Rights Case Iowa - Applicants must disclose any potential background check issues, allowing for preemptive planning and discussion of employment options.