Fill a Valid Iowa 44 019A Template

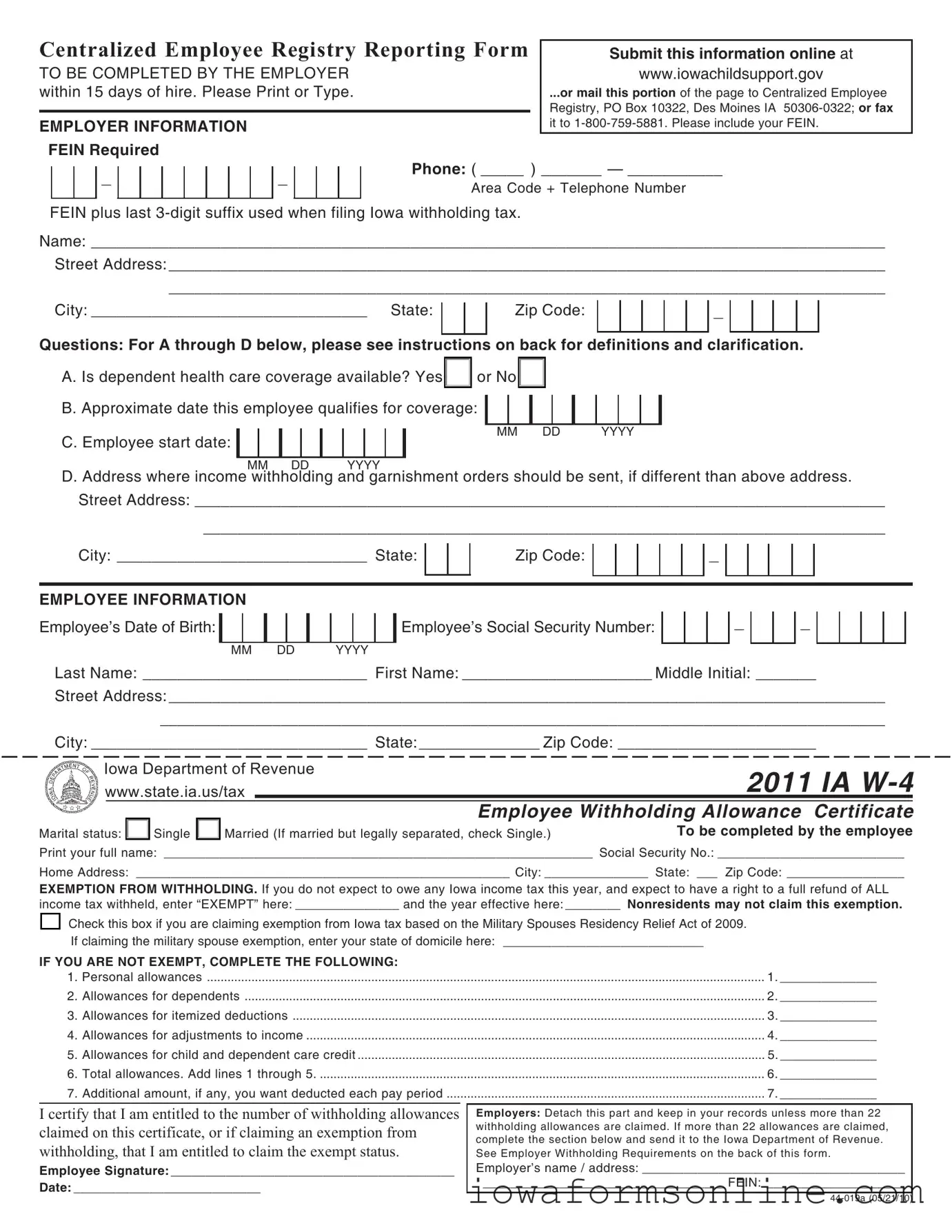

The Iowa 44 019A form serves as a crucial tool for employers in the state, ensuring compliance with employee registration and withholding requirements. This form consists of two main sections: the Centralized Employee Registry Reporting Form and the Iowa W-4 Employee Withholding Allowance Certificate. Employers must complete the first section within 15 days of hiring or rehiring an employee, providing essential information such as the employee's start date, health care coverage availability, and the address for income withholding orders. The form requires the employer's Federal Employer Identification Number (FEIN) and contact details. The second section, the Iowa W-4, allows employees to declare their withholding allowances and claim exemptions from state income tax if applicable. Employees must provide personal information, including their Social Security number and marital status, while also specifying any additional withholding amounts if necessary. This form not only facilitates accurate tax withholding but also helps maintain a centralized record of employees for child support purposes. Adhering to the guidelines set forth in the Iowa 44 019A is essential for both employers and employees to ensure compliance with state regulations.

Iowa 44 019A Preview

Centralized Employee Registry Reporting Form |

Submit this information online at |

|||||||||||||||||

TO BE COMPLETED BY THE EMPLOYER |

|

|

www.iowachildsupport.gov |

|||||||||||||||

within 15 days of hire. Please Print or Type. |

|

|

...or mail this portion of the page to Centralized Employee |

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Registry, PO Box 10322, Des Moines IA |

EMPLOYER INFORMATION |

|

|

|

|

|

|

it to |

|||||||||||

FEIN Required |

|

|

|

|

|

|

|

|||||||||||

|

|

|

_ |

|

|

|

|

|

|

|

_ |

|

|

|

Phone: ( _____ ) _______ — ___________ |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Area Code + Telephone Number |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

FEIN plus last

Name: ____________________________________________________________________________________________

Street Address: ___________________________________________________________________________________

___________________________________________________________________________________

City: ________________________________ State:

Zip Code:

_

Questions: For A through D below, please see instructions on back for definitions and clarification.

A. Is dependent health care coverage available? Yes |

|

or No |

|

|

|

|

|

|

|||||||||||||

B. Approximate date this employee qualifies for coverage: |

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C. Employee start date: |

|

|

|

|

|

|

|

|

|

|

|

MM DD |

|

YYYY |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

YYYY

D. Address where income withholding and garnishment orders should be sent, if different than above address.

Street Address: ________________________________________________________________________________

_______________________________________________________________________________

City: _____________________________ State: |

|

|

Zip Code: |

|

|

|

|

|

_ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

EMPLOYEE INFORMATION

Employee’s Date of Birth:

MM DD

Employee’s Social Security Number:

YYYY

_

_

Last Name: __________________________ First Name: ______________________ Middle Initial: _______

Street Address: ___________________________________________________________________________________

____________________________________________________________________________________

City: ________________________________ State: ______________ Zip Code: _______________________

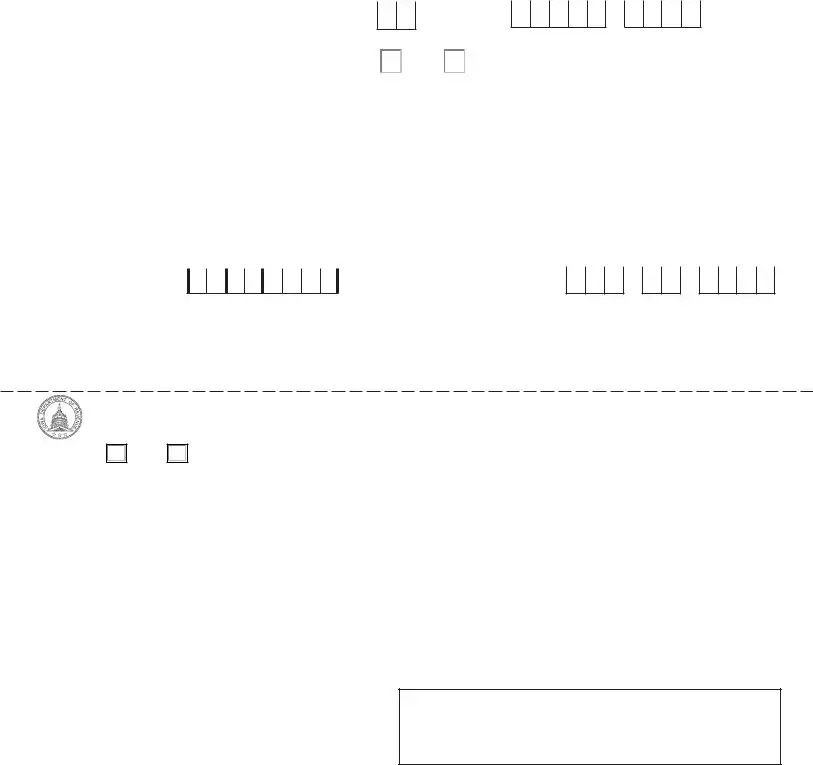

Iowa Department of Revenue |

2011 IA |

|

||||||

www.state.ia.us/tax |

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Employee Withholding Allowance Certificate |

||

|

|

|

|

|

|

|||

Marital status: |

|

Single |

|

Married (If married but legally separated, check Single.) |

To be completed by the employee |

|||

Print your full name: ______________________________________________________________ Social Security No.: ___________________________

Home Address: ______________________________________________________ City: _______________ State: ___ Zip Code: _________________

EXEMPTION FROM WITHHOLDING. If you do not expect to owe any Iowa income tax this year, and expect to have a right to a full refund of ALL income tax withheld, enter “EXEMPT” here: _______________ and the year effective here: ________ Nonresidents may not claim this exemption.

|

Check this box if you are claiming exemption from Iowa tax based on the Military Spouses Residency Relief Act of 2009. |

|

||

|

If claiming the military spouse exemption, enter your state of domicile here: _____________________________ |

|

||

IF YOU ARE NOT EXEMPT, COMPLETE THE FOLLOWING: |

|

|||

|

1. Personal allowances |

1. ______________ |

||

2. |

Allowances for dependents |

2. ______________ |

||

3. |

Allowances for itemized deductions |

3. ______________ |

||

4. |

Allowances for adjustments to income |

4. ______________ |

||

5. |

Allowances for child and dependent care credit |

5. ______________ |

||

6. |

Total allowances. Add lines 1 through 5 |

6. ______________ |

||

7. |

Additional amount, if any, you want deducted each pay period |

7. ______________ |

||

|

|

|

|

|

I certify that I am entitled to the number of withholding allowances claimed on this certificate, or if claiming an exemption from withholding, that I am entitled to claim the exempt status.

Employee Signature: _________________________________________

Date: ___________________________

Employers: Detach this part and keep in your records unless more than 22 withholding allowances are claimed. If more than 22 allowances are claimed, complete the section below and send it to the Iowa Department of Revenue. See Employer Withholding Requirements on the back of this form.

Employer’s name / address: ______________________________________

___________________________________ FEIN: ____________________

TOP PORTION OF FORM– CENTRALIZED EMPLOYEE REGISTRY REPORTING FORM – EMPLOYER REPORTING REQUIREMENTS

An employer doing business in Iowa who hires or rehires an employee must complete this section. Submit online at www.iowachildsupport.gov. You may also mail this portion of the page to Centralized Employee Registry, PO Box 10322, Des Moines IA

(EPICS) Unit at |

Questions A through D |

|

|

|

|

A. Is a family health insurance plan offered through employment? This question does not |

C. Indicate the first day for which the employee is owed |

|

relate to insurability of employee’s dependents. |

|

compensation. |

B. Example: Is dependent insurance coverage offered upon hire or after six months of |

D. This information is needed for income withholding and |

|

employment? This question does not relate to insurability of employee’s dependents. |

garnishment purposes. |

|

BOTTOM PORTION OF FORM – IA

Exemption from Withholding: You should claim exemption from withholding if you are a resident of Iowa and do not expect to owe any Iowa income tax or expect to have a right to a refund of all income tax withheld. If you qualify, write "EXEMPT" and the year exempt status is effective. Exempt guidelines are: (1) You are exempt if you will earn $5,000 or less and are claimed as a dependent on another person’s return, or (2) You are exempt if you will earn $9,000 or less and are not claimed as a dependent on another person’s return, or (3) married and both spouses’ total is less than $13,500. See your payroll officer to determine how much you expect to make in a calendar year. Nonresidents may not claim this exemption.

Under the Military Spouses Residency Relief Act of 2009, you may be exempt from Iowa income tax on your wages if (1) your spouse is a member of the armed forces present in Iowa in compliance with military orders; (2) you are present in Iowa solely to be with your spouse; and (3) you maintain your domicile in another state. If you claim this exemption, check the appropriate box, enter the state other than Iowa you are claiming as your state of domicile, and attach a copy of your spousal military identification card to the IA

Taxpayers 65 years of age or older: You are exempt if you are single and your income is $24,000 or less or if you are married and your combined income is $32,000 or less. Only one spouse must be 65 or older to qualify for the exemption.

You must complete a new

FILING REQUIREMENTS/NUMBER OF ALLOWANCES

Each employee must file this Iowa

1.Personal Allowances: You can claim the following personal allowances:

•1 allowance for yourself or 2 allowances if you are unmarried and eligible to claim head of household status, plus 1 allowance if you are 65 or older, and plus 1 allowance if you are blind.

•If you are married and your spouse either does not work or is not claiming his/her allowances on a separate

•If you are single and hold more than one job, you may not claim the same allowances with more than one employer at the same time. If you are married and both you and your spouse are employed, you may not both claim the same allowances with both of your employers at the same time.

•To have the highest amount of tax withheld, claim "0" allowances on line 1.

2.Allowances for Dependents: You may claim 1 allowance for each dependent you will be able to claim on your Iowa income tax return.

3.Allowances for Itemized Deductions

(a)Enter total amount of estimated itemized deductions ..................................................................................... (a) $ _________________

(b)Enter amount of your standard deduction using the following information ................................................... (b) $ _________________

If single, married filing separately on a combined return, or married filing separate returns, enter $1,830 If married filing a joint return, unmarried head of household, or qualifying widow(er), enter $4,500

(c)Subtract line (b) from line (a) and enter the difference or zero, whichever is greater.................................... (c) $ _________________

(d)Additional allowance: Divide the amount on line (c) by $600, round to the nearest whole number and enter on line 3 of the IA

4.Allowances for Adjustments to Income: Estimate allowable adjustments to income for payments to an IRA, Keogh, or SEP; penalty on early withdrawal of savings; alimony paid; moving expense deduction from federal form 3903; and student loan interest, which are reflected on the Iowa 1040 form. Divide this amount by $600, round to the nearest whole number, and enter on line 4 of the IA

5.Allowances for Child/Dependent Care Credit: Persons having child/dependent care expenses qualifying for the federal and Iowa Child and Dependent Care Credit may claim additional Iowa withholding allowances based on their net incomes. If you have qualifying child and dependent care expenses and wish to reduce your Iowa withholding on the basis of this credit, you may claim additional withholding allowances for Iowa based on the following table. Married persons, regardless of their expected Iowa filing status, must calculate their withholding allowances based on their combined net incomes. Note that if net income is $45,000 or more, no withholding allowances are allowed for the Child and Dependent Care Credit, as taxpayers with these incomes are not eligible for the Iowa Child and Dependent Care Credit.

Withholding Allowances Allowed: IOWA NET INCOME |

ALLOWANCES |

IOWA NET INCOME |

ALLOWANCES |

IOWA NET INCOME |

ALLOWANCES |

$0 - $20,000 |

5 |

$20,000- $30,000 |

4 |

$30,000 - $44,999 |

3 |

Enter the number of allowances on line 5 of the IA

6.Total: Enter total of lines 1 through 5.

7.Additional Amount of Withholding Deducted: If you are not having enough tax withheld, you may request your employer to withhold more by filling in an additional amount on line 7. Often married couples, both of whom are working, and persons with two or more jobs need to have additional tax withheld. You may also need to have additional tax withheld because you have income other than wages, such as interest and dividends, capital gain, rents, alimony received, etc. Estimate the amount you will be

Changes in Allowances: You may file a new

Penalties: Penalties apply for willfully supplying false information or for willful failure to supply information which would reduce the withholding allowances. If you file as exempt from withholding and you incur an income tax liability, you may be subject to a penalty for underpayment of estimated tax. Employer Withholding Requirements: The employer must maintain records of the

Document Attributes

| Fact Name | Details |

|---|---|

| Form Purpose | The Iowa 44 019A form serves as the Centralized Employee Registry Reporting Form, which employers must complete when hiring or rehiring employees. |

| Submission Deadline | Employers are required to submit the form within 15 days of the employee's hire date. |

| Submission Methods | The form can be submitted online at www.iowachildsupport.gov, mailed to a designated address, or faxed to a specified number. |

| Required Information | Employers must provide their Federal Employer Identification Number (FEIN), along with employee details such as name, address, and Social Security Number. |

| Health Coverage Inquiry | The form includes questions regarding the availability of dependent health care coverage for the employee. |

| Governing Law | This form is governed by Iowa Code Chapter 252E, which outlines the requirements for employee registry reporting in the state. |

Popular PDF Forms

Iowa Universal Application - Finally, the Iowa Universal Application demonstrates how technology can facilitate more efficient and user-centric government services.

A Texas Last Will and Testament form is a legal document that outlines how a person's assets will be distributed after their death. This form ensures that your wishes are honored and provides clarity for your loved ones during a difficult time. To get started on securing your legacy, you can find the necessary documentation at Texas Documents and fill out the form by clicking the button below.

Iowa Dot Permit - This document is crafted to assist Iowa residents in fulfilling state requirements through a structured information framework.